TRG | The Bottom Line – 4/17

This week, TRG published our Q1’26 Residential & Non-Residential Products & Services Survey, focusing on end-market demand, the outlook for the year, and expectations for company guidance.

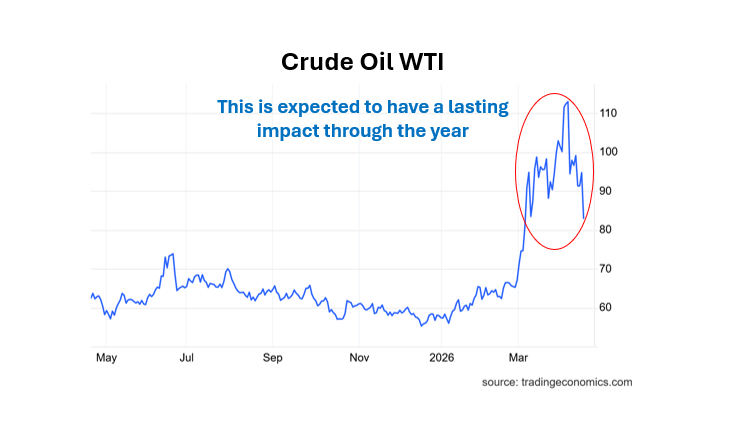

We believe residential housing remains in a holding pattern and expect this to persist through 2026. For companies with greater residential exposure, we see a meaningful probability of reduced full-year guidance with Q1 earnings, driven by several compounding factors. These include weather-related disruptions across the U.S. that limited construction and retail activity, continued weakness in consumer confidence, and interest rates that are unlikely to see significant cuts in the near term. Additionally, inflationary pressures from higher input costs (as indicated by recent supplier pricing actions, including chemical providers) are expected to flow through in the coming weeks and months.

Non-residential demand remains bifurcated. Local projects are expected to stay sluggish, consistent with trends over the past several years, and our view aligns with signals from the ABI. In contrast, megaproject activity remains resilient and continues to grow, and we expect this segment to remain robust for the foreseeable future.

Disclosure: This content reflects the independent views of Thompson Research Group, LLC (“TRG”), is provided for informational purposes only, and does not constitute an offer or solicitation to buy or sell any security. Additional information, including analyst certification and compensation-related conflicts of interest, may be found here: (disclosures).