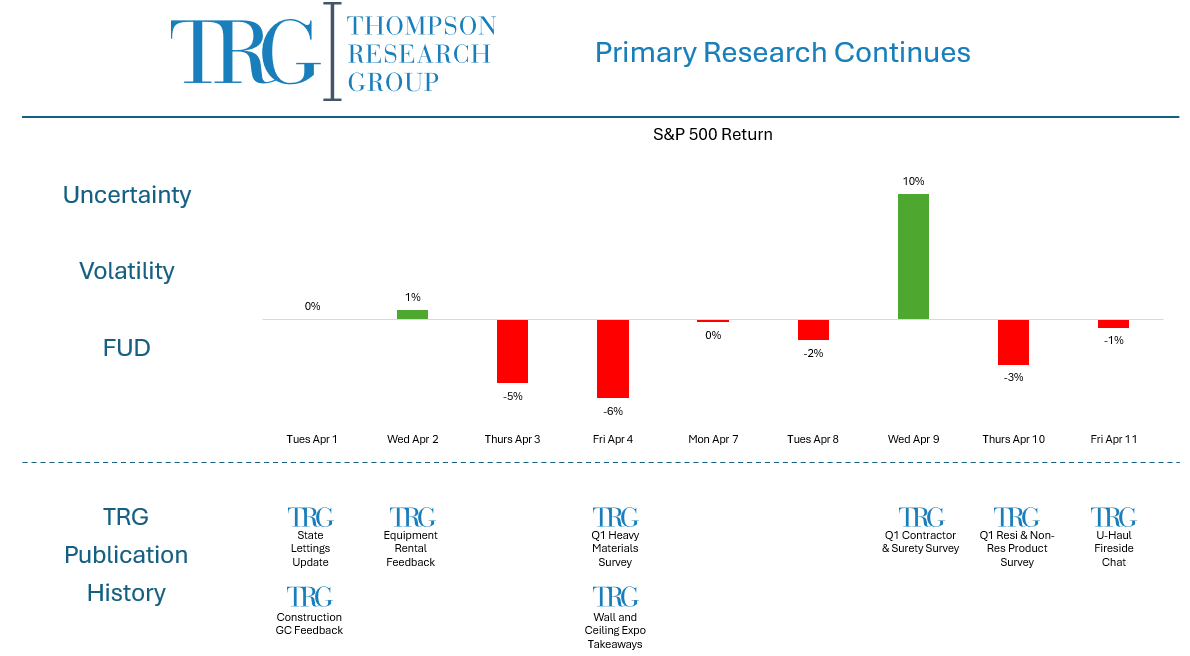

TRG | The Bottom Line – 4/11

Uncertainty is perhaps at all-time-highs, yet we at TRG are still tasked with analyzing the world and our client base still has to operate businesses and make investment decisions. Now more than ever primary research stands out as a differentiator and value add in understanding the economic outlook. Coincidentally, primary research is and has been the cornerstone of TRG’s research process, providing real-time and on-the-ground insights into the world in which we cover. This week included 2 industry surveys across TRG’s coverage universe, an earnings pre-release from Martin Marietta, and a fireside chat with U-Haul, providing a broad readthrough on the construction supply chain. While many survey responses include some sort of “Who knows” disclaimer, it is the amalgamation of these conversations that help inform TRG’s view on the world.

Our broad long-term view largely remains the same, with the construction industry in a “slower for longer” scenario. Non-res construction remains divergent with good trends in manufacturing and data centers offset by office and light commercial. Resi construction is pressured by rates and affordability but continues at a steady level given big builder buydowns and necessity. Uncertainty could lead to delayed investment spending in some areas. But, industry feedback on non-res construction is not showing delays or cancellations broadly. To carry an analogy, the music continues despite all the noise. We will continue to monitor if the music keeps playing at the same volume. Our primary research continues next week with TRG’s Q1 Equipment Rental Survey and other timely feedback and insights as we navigate this investment landscape.