TRG | The Bottom Line – 5/15

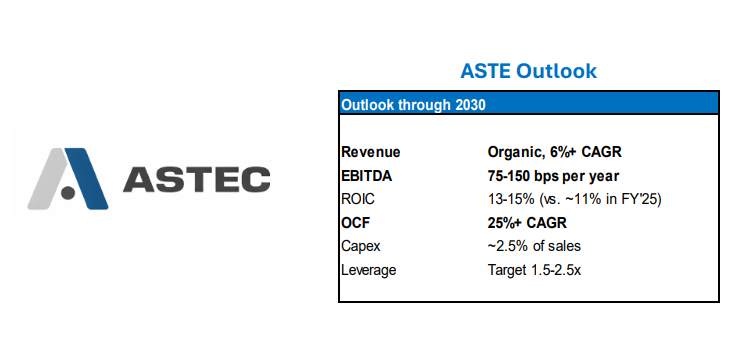

Einstein famously said that compound interest is the 8th wonder of the world. At Wednesday's virtual investor event, Astec laid out their long-term growth targets of organic sales CAGR of 6% and 25%+ CAGR of operating cash flow through 2030. This is supported by annual EBITDA margin expansion of 75-150 bps, which implies an EBITDA margin of 14-17% in 2030 (vs. 10% in FY’25). Other key factors include: Astec targets part & service mix of 40-50% of total revenue (vs. 34% in FY’25 and ~33% in FY’23-24). Astec can create excess capital capacity of $400-600MM, which they hope can be deployed to accretive M&A.

TRG Perspective – Amongst industrial stocks, there are not many companies that have the realistic potential to compound operating cash flow by 25% per annum for many years. We believe that Astec has trodden far down the transformation path. At this juncture of the journey, we see a compounding on already achieved success that enables greater aspirations. Investors who like the “infrastructure + reindustrialization theme” are looking at an opportunity set with many stocks that have already moved up significantly or companies who are already highly optimized. Astec is a beneficiary of these themes, but is in the early stages of optimization. We believe the current valuation is quite cheap (6.5x EV/EBITDA vs. our FY’27 estimate) and the EBITDA margin translation to high cash flow growth is a compelling story.

Disclosure: This content reflects the independent views of Thompson Research Group, LLC (“TRG”), is provided for informational purposes only, and does not constitute an offer or solicitation to buy or sell any security. Additional information, including analyst certification and compensation-related conflicts of interest, may be found here: (disclosures).